When Home Shopping Meant Driving Blind: The Real Estate Hunt Before Online Listings

When Home Shopping Meant Driving Blind: The Real Estate Hunt Before Online Listings

Picture this: It's Saturday morning in 1985, and you're house hunting. Your toolkit consists of yesterday's newspaper classified section, a tank of gas, and the business card of a real estate agent who may or may not call you back. You have no idea what most houses look like inside, no clue about neighborhood crime rates, and absolutely zero ability to research comparable sales prices. Welcome to home buying in pre-internet America, where purchasing the largest investment of your life required more blind faith than a skydiving lesson.

The Great Information Blackout

Before Zillow, Realtor.com, and Redfin transformed house hunting into a digital sport, buyers operated in an information vacuum that would seem impossible today. Want to know what your neighbor paid for their house last year? Good luck. Curious about local school ratings? Hope you know someone who lives there. Interested in seeing more than one grainy black-and-white photo of a property? You'd better be ready to drive.

The Multiple Listing Service (MLS) existed, but it was the exclusive domain of licensed real estate professionals. This created a system where agents held all the cards, and buyers had to trust their judgment completely. There was no way to verify if the "charming fixer-upper" was actually a money pit, or if the "up-and-coming neighborhood" was genuinely improving or just expensive wishful thinking.

The Sunday Drive Ritual

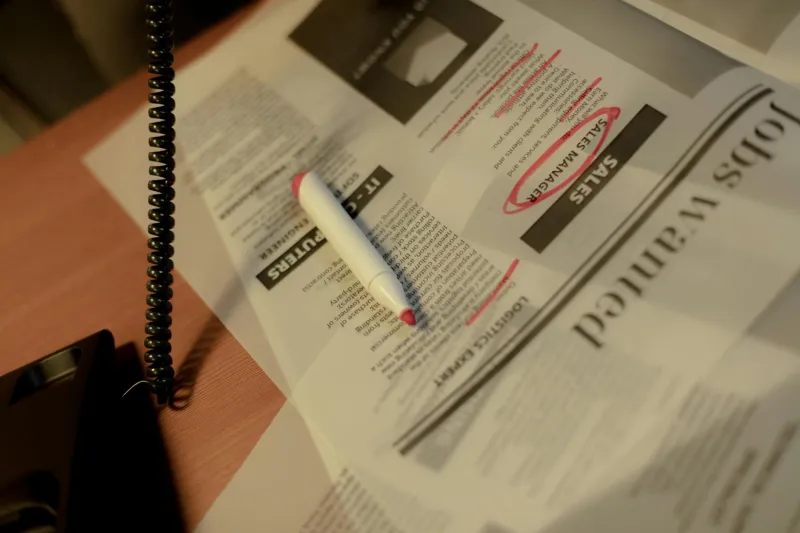

Weekends in house-hunting families followed a predictable pattern. Dad would spread the newspaper across the kitchen table, circling addresses in red pen while Mom called the phone numbers listed in tiny print. Most of the time, you'd get a busy signal or an answering machine. When you did reach someone, they'd give you an address and maybe—if you were lucky—a time when the house would be shown.

Then came the driving. Lots of driving. Armed with a road atlas and handwritten directions, families would spend entire Saturdays navigating to houses that might not even be available anymore. Real estate agents couldn't update listings in real-time, so you'd frequently arrive at properties that had been sold days earlier, with only a "SOLD" sign to show for your gas money and optimism.

The Agent as Gatekeeper

In this pre-digital world, real estate agents wielded enormous power. They controlled access to information, managed the entire viewing process, and essentially served as the sole bridge between buyers and sellers. Unlike today's system where buyers can research properties independently and even schedule their own showings, everything flowed through the agent.

This created some interesting dynamics. Good agents were worth their weight in gold—they knew the neighborhoods, had insider information about upcoming listings, and could navigate the complex paperwork maze. Bad agents could make your life miserable, showing you overpriced dumps while the perfect house sold to someone else's client.

The Paperwork Mountain

If finding a house was complicated, actually buying one was a bureaucratic nightmare that makes today's process look streamlined. Every document had to be physically signed, notarized, and mailed or hand-delivered. Mortgage applications were typewritten forms filled out in person at bank branches, where loan officers would spend weeks manually verifying every detail of your financial life.

Title searches required lawyers to physically visit courthouses and dig through paper records. Home inspections were scheduled through phone calls, and the results arrived as typewritten reports in manila envelopes. Want to compare mortgage rates? That meant visiting multiple banks in person and collecting rate sheets that might be outdated by the time you got home.

The Closing Day Mystery

Perhaps nothing illustrates the old system's opacity better than closing day itself. Buyers would arrive at a lawyer's office or title company with little more than a rough estimate of what they'd owe. The final numbers—closing costs, exact loan terms, prorated taxes—were often mysteries until the moment you sat down to sign.

There was no three-day review period, no detailed closing disclosure delivered in advance. You showed up with a cashier's check for an approximate amount and hoped the math worked out. If it didn't, you scrambled to get additional funds or renegotiate on the spot.

What We Lost (And What We Gained)

Today's home buyers can browse thousands of listings from their couch, take virtual tours, research neighborhood statistics, compare mortgage rates online, and even get pre-approved for loans through smartphone apps. The entire process, while still complex, is dramatically more transparent and buyer-friendly.

But something was lost in this digital transformation. The old system, for all its inefficiencies, created deeper relationships between agents and clients. When information was scarce, trust mattered more. Agents had to earn their commissions through local knowledge and personal service rather than just facilitating online research.

The Modern Perspective

Looking back, it's remarkable that anyone successfully bought a house in the pre-internet era. The combination of limited information, manual processes, and complete dependence on professionals created a system that was both inefficient and expensive. Yet millions of Americans navigated this maze and achieved homeownership, armed with nothing but determination and a willingness to drive around on weekends.

Today's house hunters, spoiled by instant information and digital convenience, might struggle to imagine a world where buying a home required such blind faith. But perhaps that faith, combined with simpler expectations and stronger community connections, made the journey more meaningful—even if it took a lot more gas money to get there.